The 50/30/20 Budget Explained

By Darwin Lee on June 25, 2026

Budgeting often sounds more complicated than it needs to be. Many people imagine spreadsheets filled with dozens of categories, daily expense tracking, and strict spending rules that are difficult to maintain.

The 50/30/20 budget offers a simpler approach. Instead of tracking every dollar in detail, it divides your income into three broad categories: needs, wants, and savings.

Its popularity comes from its simplicity. The framework is easy to understand, flexible enough for different lifestyles, and provides a balanced way to manage money without feeling overly restrictive.

What is the 50/30/20 budget?

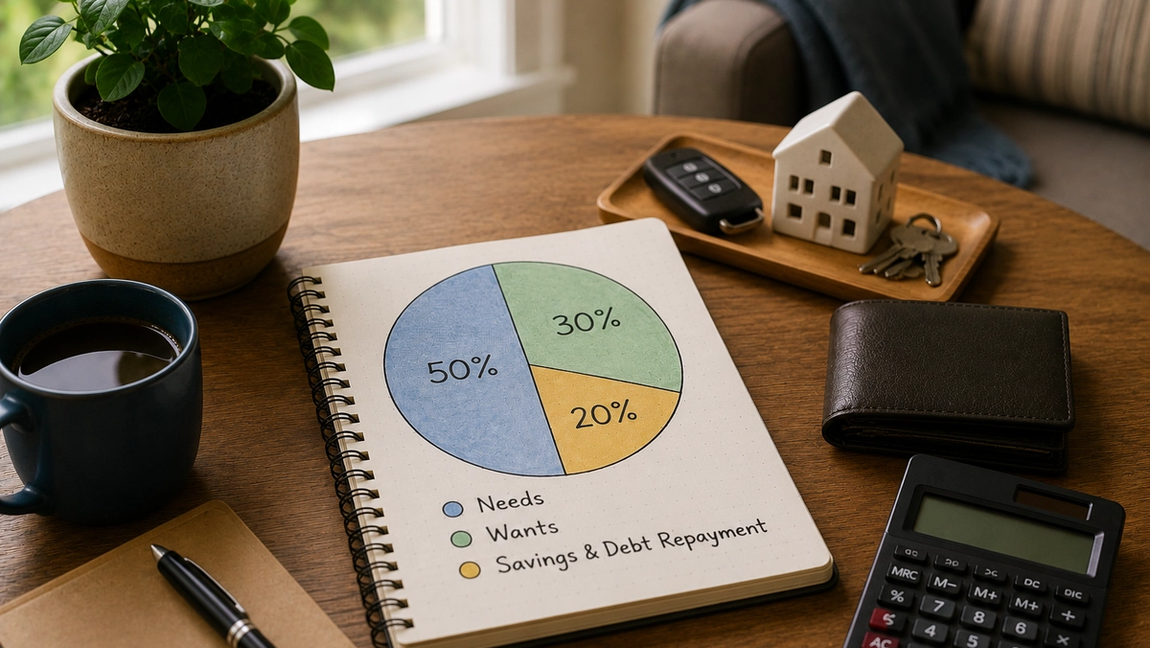

The 50/30/20 budget is a budgeting guideline that suggests allocating your after-tax income as follows:

- 50% for needs

- 30% for wants

- 20% for savings and debt repayment

Rather than focusing on dozens of spending categories, the method encourages you to think about where your money is going at a higher level.

The goal isn’t to follow the percentages perfectly every month. Instead, it’s to create a healthy balance between current expenses, personal enjoyment, and future financial security.

For many people, this approach feels less overwhelming than traditional budgeting methods.

The 50% category: Needs

Needs are the expenses required to maintain your basic standard of living.

These are costs you would generally struggle to avoid without significantly affecting your daily life. Common examples include:

- Housing or rent

- Utilities

- Groceries

- Transportation

- Insurance

- Minimum debt payments

- Essential healthcare expenses

The key question is whether the expense is necessary rather than optional.

For example, housing is a need, but upgrading to a larger apartment than you require may partially fall into the wants category. Similarly, groceries are a need, while frequent restaurant meals are generally considered wants.

If your essential expenses exceed 50% of your income, it doesn’t mean you’ve failed. In many areas with high housing costs, reaching the 50% target can be challenging. The percentages are guidelines rather than strict rules.

The 30% category: Wants

This category covers spending that improves your quality of life but isn’t strictly necessary.

Examples include:

- Dining out

- Streaming services

- Entertainment

- Travel

- Hobbies

- Gym memberships

- Shopping beyond basic necessities

- Upgraded technology or gadgets

The wants category is often where people feel guilty when budgeting. However, the 50/30/20 method intentionally includes room for enjoyment.

A sustainable budget should allow you to spend money on things that bring happiness and fulfillment. The goal isn’t to eliminate discretionary spending but to keep it within reasonable limits.

Many budgeting plans fail because they leave no room for fun. The 30% allocation recognizes that enjoying your money is an important part of financial well-being.

The 20% category: Savings and debt repayment

The final 20% is dedicated to building your financial future.

This category can include:

- Emergency fund contributions

- Retirement savings

- Investment accounts

- Additional debt payments beyond minimum requirements

- Saving for major future goals

- Education funds

- Home down payment savings

This portion of the budget is what helps create long-term financial security.

While spending categories often provide immediate satisfaction, savings and investments create options and flexibility later. Over time, this category can reduce financial stress and help you achieve major life goals.

Even if you can’t reach the full 20% immediately, consistently saving something is often more important than waiting until you can save the ideal amount.

Why people like the 50/30/20 method

One of the biggest advantages of this budget is its simplicity.

Many people abandon detailed budgets because tracking every purchase becomes exhausting. The 50/30/20 approach focuses on broad spending patterns rather than individual transactions.

It also promotes balance.

Some budgeting methods prioritize saving so aggressively that people feel deprived. Others focus heavily on current spending while neglecting future goals. The 50/30/20 framework attempts to create a middle ground where you can enjoy life today while still preparing for tomorrow.

For many people, that balance makes the system easier to maintain long term.

When the percentages don’t fit perfectly

The reality is that not everyone’s finances fit neatly into these percentages.

Someone living in an expensive city may spend more than 50% of their income on housing and essential expenses. A person paying off significant debt may allocate much more than 20% toward repayment. Others may choose to save aggressively and spend less on wants.

That’s perfectly normal.

The strength of the 50/30/20 budget lies in its flexibility. Think of it as a starting point rather than a rulebook. The exact percentages can be adjusted to fit your circumstances and priorities.

What’s most important is understanding where your money is going and ensuring that savings remain part of the equation.

A framework, not a restriction

The 50/30/20 budget works because it’s simple enough for most people to follow without feeling overwhelmed.

It encourages you to cover your essentials, enjoy your life, and build financial security at the same time. Rather than obsessing over every purchase, it focuses on maintaining a healthy overall balance.

No budgeting method is perfect for everyone, but the 50/30/20 approach offers a practical starting point for people who want greater control over their finances without turning money management into a full-time job.

At its core, the idea is straightforward: take care of your needs, make room for the things you enjoy, and consistently invest in your future. When those three areas are in balance, managing money becomes much simpler—and often much less stressful.